Weekly Market Commentary – 5/7/2021

-Darren Leavitt, CFA

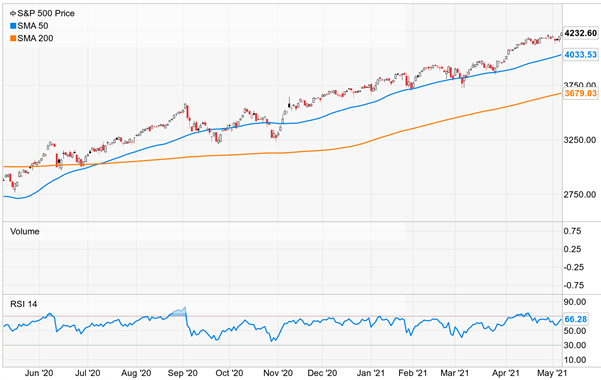

US equity indices finished the week mixed as a strong rotational trade into cyclicals and out of high growth technology issues reappeared. The S&P 500 and Dow forged new all-time highs as the tech-heavy NASDAQ and Russell 2000 lagged. Energy, Financials, Materials, and Industrial sectors outperformed over the week while the Information Technology and Consumer Discretionary sectors underperformed. Q1 earnings results continued to roll in better than expected, but in most cases, the results were overshadowed by the prominent rotational trade. Economic news for the week was much weaker than expected, which caught many by surprise.

For the week, the S&P 500 gained 1.2%, the Dow added 2.7%, the NASDAQ declined 1.5%, and the Russell 2000 eked out a 0.2% increase. The US Treasury curve continued to flatten, with the 2-year yield falling two basis points to close at 0.14% and the 10-year bond yield shedding five basis points to 1.58%. Interestingly, the lower move in yields did not act as a buoy for growth stocks. Gold prices rose 3.5% or $62.90 to close at 1830.80. Oil prices ticked higher by 2.2%, with WTI closing at $64.94 a barrel.

The much anticipated April Employment situation report was a big disappointment. The headline non-farm payrolls number came in at 266k versus a consensus estimate of 1 million. Lower revisions for the March report accompanied the big miss. The unemployment rate ticked higher coming in at 6.1% versus the Street estimate of 5.8%. The news generated questions regarding the effects that extended and supplemental unemployment benefits have on the labor market. The Biden administration dismissed the correlation and suggested that the miss prompt Congress install his 1.8 trillion dollar American Family Plan quickly. ISM Manufacturing and Services data also regressed but still showed both parts of the economy in expansion. April ISM Manufacturing came in at 60.7 less than the consensus of 65.3 and down from the prior month’s reading of 64.7. ISM Non-Manufacturing came in at 62.7 versus the street estimate of 65 and down from the March reading of 63.7.

The information in this Market Commentary is for general informational and educational purposes only. Unless otherwise stated, all information and opinion contained in these materials were produced by Foundations Investment Advisers, LLC (“FIA”) and other publicly available sources believed to be accurate and reliable. No representations are made by FIA or its affiliates as to the informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation. No party, including but not limited to, FIA and its affiliates, assumes liability for any loss or damage resulting from errors or omissions or reliance on or use of this material.

The views and opinions expressed are those of the authors do not necessarily reflect the official policy or position of FIA or its affiliates. Information presented is believed to be current, but may change at any time and without notice. It should not be viewed as personalized investment advice. All expressions of opinion reflect the judgment of the authors on the date of publication and may change in response to market conditions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. You should consult with a professional advisor before implementing any strategies discussed. Content should not be viewed as an offer to buy or sell any of the securities mentioned or as legal or tax advice. You should always consult an attorney or tax professional regarding your specific legal or tax situation. Investment advisory services are offered through Foundations Investment Advisors, LLC, an SEC registered investment adviser.

Jim E. Sloan is the founder of Jim Sloan & Associates, LLC, a comprehensive wealth management firm located in The Woodlands, Texas. Jim is an Investment Adviser Representative providing investment advisory services through AE Wealth Management, LLC, an *SEC Registered Investment advisor. This relationship allows Jim Sloan & Associates, LLC to bring institutional-level experience, practices, and pricing to individual families. Jim is also a licensed insurance agent in Colorado and Texas. This is Jim’s sixth financial book and is aimed at helping investors become financially informed. Jim is a U.S. Army veteran, native Houstonian, and lives in the Woodlands, volunteers with several local charities, believes in the name of Jesus, loves to travel, and enjoys most things outdoors.

Jim E. Sloan is the founder of Jim Sloan & Associates, LLC, a comprehensive wealth management firm located in The Woodlands, Texas. Jim is an Investment Adviser Representative providing investment advisory services through AE Wealth Management, LLC, an *SEC Registered Investment advisor. This relationship allows Jim Sloan & Associates, LLC to bring institutional-level experience, practices, and pricing to individual families. Jim is also a licensed insurance agent in Colorado and Texas. This is Jim’s sixth financial book and is aimed at helping investors become financially informed. Jim is a U.S. Army veteran, native Houstonian, and lives in the Woodlands, volunteers with several local charities, believes in the name of Jesus, loves to travel, and enjoys most things outdoors.